I’ve been a health advisor for several years now. When I first started, my personal needs were different from what it is now. I operated on a smaller scale and had limited resources, barely a budget. You know how it is right? You’ve been there.

Today, my small business is starting to grow. I’ve turned a corner in my entrepreneurial journey. I have a list of go-to partnerships, my team is expanding and I’m making plans to scale the operations and venture both vertically and laterally.

This business treatment applies to any typical small business. We start slowly and then eventually move into the growth or expansion phase. We hire more help, we have access to more funds to invest back into the business.

It doesn’t matter which part of the country you’re in – Texas, Oklahoma or Florida – small businesses across the United States of America grow in different ways.

Yet, in all stages of growth, small business owners have to consider and remember the importance of health insurance for themselves. Aside from getting insurance for your team or your business operations, you need health insurance to ensure you are protected from inflated medical bills should you fall ill. That “worst case scenario” protection. Oftentimes, this is neglected.

Health insurance tends to be an afterthought for many small business owners, especially with a small team.

More so, if those team members are also 1099 contract employees. Does this sound like you? Read on to know more about the best health insurance options for entrepreneurs or small businesses in this situation.

Or, listen to this podcast episode where I talk to host, Shawn Dean about the importance of health insurance for entrepreneurs and why it’s so often left neglected.

What kind of health insurance plan fits you best?

You can assess the best kind of health insurance for entrepreneurs like yourself depending on the stage your business is currently in. The reason? Your income ceiling, and to reap the benefits of specific types of insurance packages.

Launch stage; lower income

Let’s say you’ve just started your small business. The situation you’re going through now will be different than that you will face in the next 5 to 10 years.

When you start, your income is lower. In this case, you might want to lock in an insurance plan that is more based on that lower income.

Health insurance options at the startup stage when entrepreneurs have very limited funds can be explored at the healthcare marketplace for a state-sponsored market health plan. The healthcare marketplace will offer tax credits or subsidies to offset that lower income. These subsidized rates can lower your premiums significantly.

However, be careful here, because as your operations grow, and your income increases more than what you estimated, you might owe the IRS in back premiums.

You can find more information on marketplace offerings at healthcare.gov or healthsherpa.com which is a user friendly version of the same.

Here is my unique link to your state’s healthcare marketplace options.

Growth stage; higher income

Once your small business grows or your revenue exceeds projected income (good on you!), you will end up owing the government in premiums. Health insurance plans at this stage can get extremely expensive, sometimes even more than a mortgage payment on a house!

When your business is doing well and growing, it is wise to switch to a health-based private plan. A health-based private plan will lock in a rate based on your current health condition so even as your income goes up, your health insurance premiums do not. This is certainly not the only option, as the private market for health insurance offers a candyland of plan options at various price points and coverage level.

However, I sincerely believe that a health-based medically underwritten health policy is truly the best for value. In fact, it’s the only type of plan I will work with! And I believe in it so much, I offer personal concierge services to all my clients on these kinds of plans. I am here standby, to help utilize and maximize the use of the plan, for the life of the policy.

Let’s see if you would be a good fit for a health-based health insurance plan- click here to get a QUOTE IN 15 MINUTES.

Questions to ask before you sign up for a health insurance plan

Here’s what you need: personal health insurance that is suitable for the stage your small business is in.

To know which is the best plan to get, you need to ask the right questions. Some of which include:

- What are the premiums you can afford?

- What is the coverage you are expecting out of the plan you choose?

- Do you need any specialized, specific medical care, such as maternity coverage?

- Does it make sense for you to get a different plan than that your spouse?

The best way to do this is by speaking to a health insurance specialist – and to do it ASAP to secure the best rates as early as possible. Don’t wait for your small business to grow before considering health insurance.

The early bird gets the juiciest worm.

How do you know when to get a private health-based plan? Use the 2020-2021 federal poverty guidelines to aid you. If your business is making 300-400% above the federal poverty level, it’s time to switch to a private plan. Not sure? I’m happy to help guide you. Book a 15 minute consult call with me.

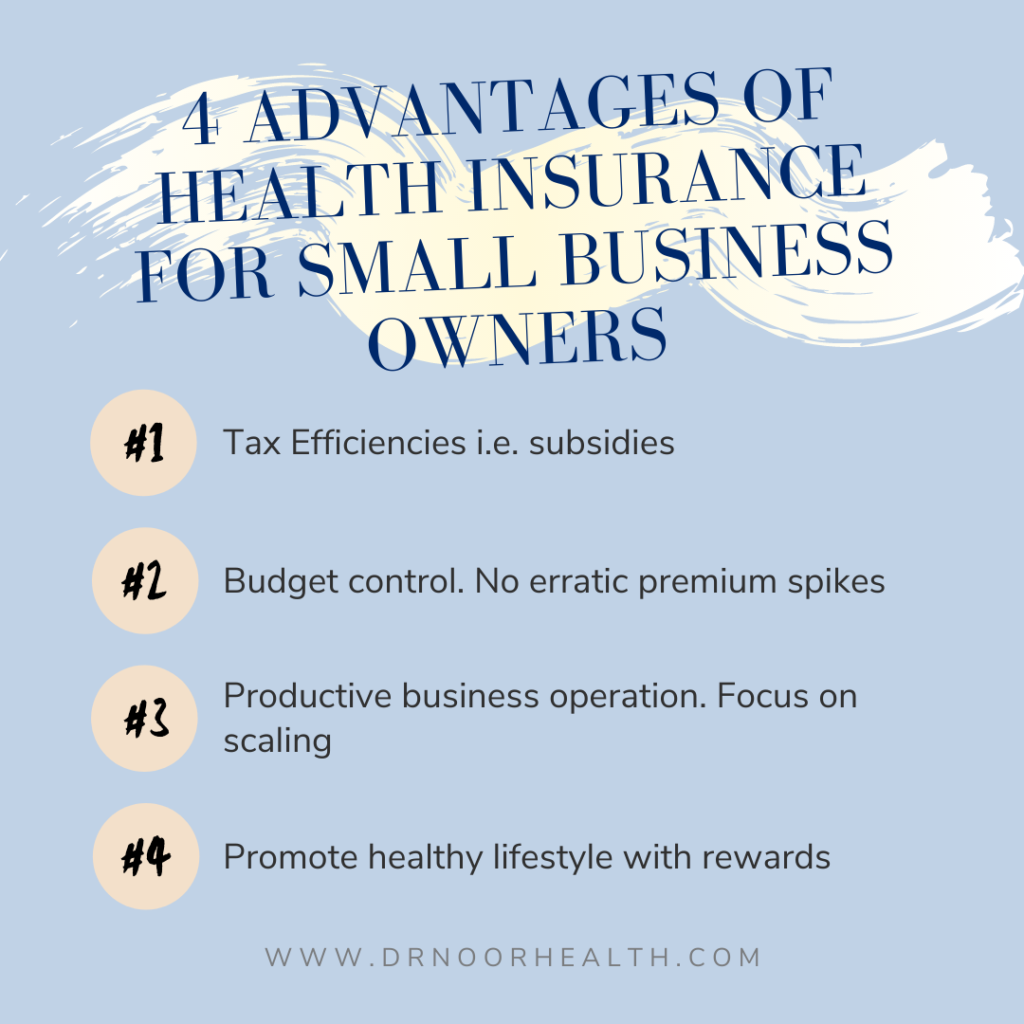

Advantages of having the right type of small business health insurance:

Health insurance can be beneficial in more than one way for small business owners.

Whatever your situation, I’m here to help figure out your best small business health insurance plan.

Check out more information and free resources HERE.